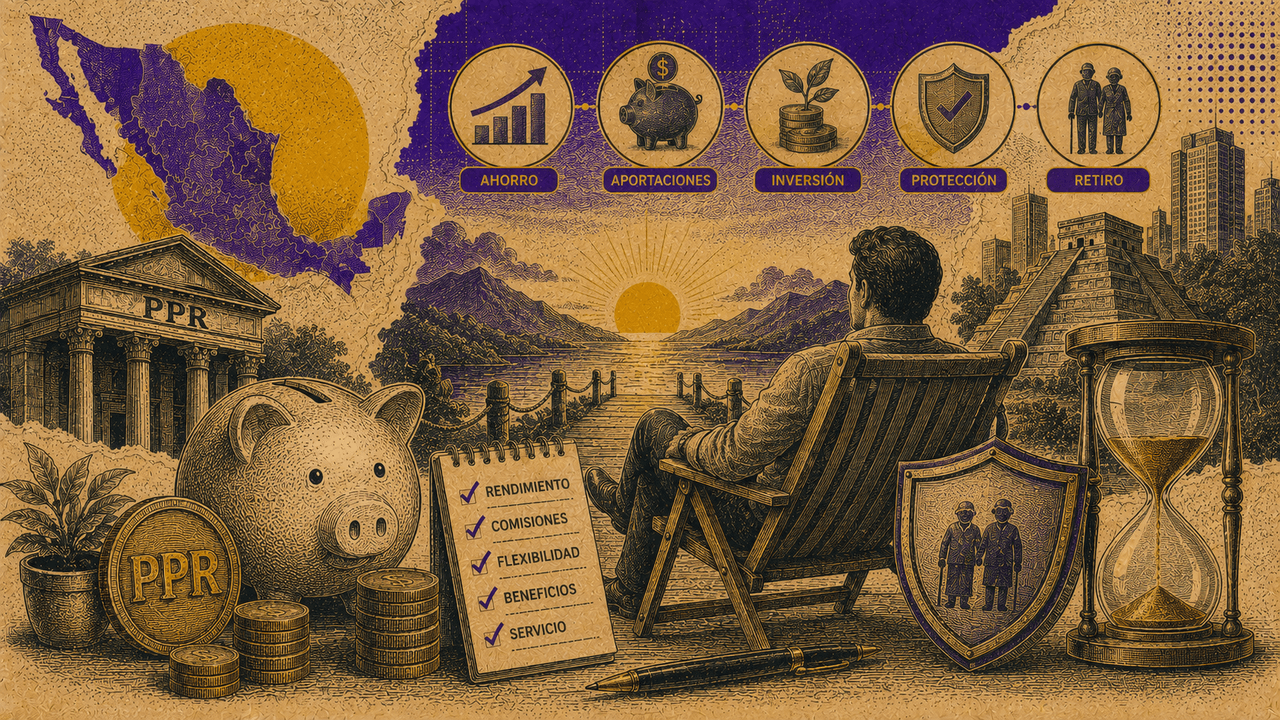

A Personal Retirement Plan - known in Mexico as a Plan Personal de Retiro or PPR - is one of the few tools available to Mexicans that lets you save for the future and pay less tax at the same time. The idea is simple: you open a voluntary account, contribute money during the year, and on your annual tax return you can deduct those contributions, which lowers the income tax (ISR) you owe or generates a refund in your favor. In exchange, it is a long-term commitment. This guide explains, without jargon, what a PPR is, how its tax benefit works, how it differs from your AFORE, and how to choose one without overpaying on fees. It is educational information, not a recommendation to buy any particular product.

The four things to know before you open one

A PPR (Plan Personal de Retiro) is a voluntary retirement savings account with a tax benefit: what you contribute can be deducted from your taxes.

You can deduct your contributions up to the lower of two limits: 10% of your annual income, or 5 UMA per year (roughly 213,900 MXN in 2026 - always confirm the current figure).

It is a long-term product designed for retirement at age 65. If you withdraw the money early, you lose the tax benefit and pay ISR.

Not all PPRs are the same. Fees vary enormously, especially in insurance-linked plans, and comparing them is what most affects your returns.

What exactly is a PPR?

A PPR is a long-term investment account created specifically for retirement, offered by banks, insurers, brokerages, and investment platforms. What sets it apart from an ordinary investment account is its tax treatment: the contributions you make are tax-deductible within certain limits, as long as you respect the plan's rules - primarily, not withdrawing the money before retirement.

Inside the PPR, your money is invested across different instruments depending on the plan you choose, from conservative debt to equities, with the goal of growing over the years. It is, in essence, a government incentive for Mexicans to voluntarily save for old age. The engine that makes it work over decades is compound interest - the returns your contributions earn go on to earn returns of their own.

How does the PPR tax benefit work?

This is the heart of the PPR. Contributions to a Personal Retirement Plan are deductible from ISR on your annual tax return, in line with Mexico's Income Tax Law (Ley del Impuesto Sobre la Renta). The deduction is capped at the lower of two amounts.

5 UMA per year (five times the annual value of the Unidad de Medida y Actualización), which in 2026 works out to roughly 213,900 MXN - an approximate figure, so verify the current UMA value.

In practice, this means that if you contribute money to your PPR during the year, when you file your annual return (in April) you can subtract those contributions from your taxable income. The result is usually a balance in your favor: money the SAT returns to you. Put differently, part of what you save is effectively handed back by the tax authority in the form of a lower tax bill.

The way this deduction interacts with your other personal deductions - medical expenses, tuition, and so on - has specific rules and limits. Before calculating your exact benefit, it is worth reviewing it with an accountant.

PPR or AFORE: what is the difference?

This is a common source of confusion, because both are meant for retirement. The key difference: your AFORE is your mandatory account, while the PPR is separate, voluntary savings. The table below sums it up.

A point many people miss: voluntary contributions made for retirement purposes inside your AFORE can also be deductible, just like a PPR. So it is not strictly an either-or choice; these are vehicles that can complement each other. The PPR usually offers more investment flexibility, while the AFORE offers the convenience of keeping everything in one place. Spreading your long-term savings sensibly is a form of diversification in its own right.

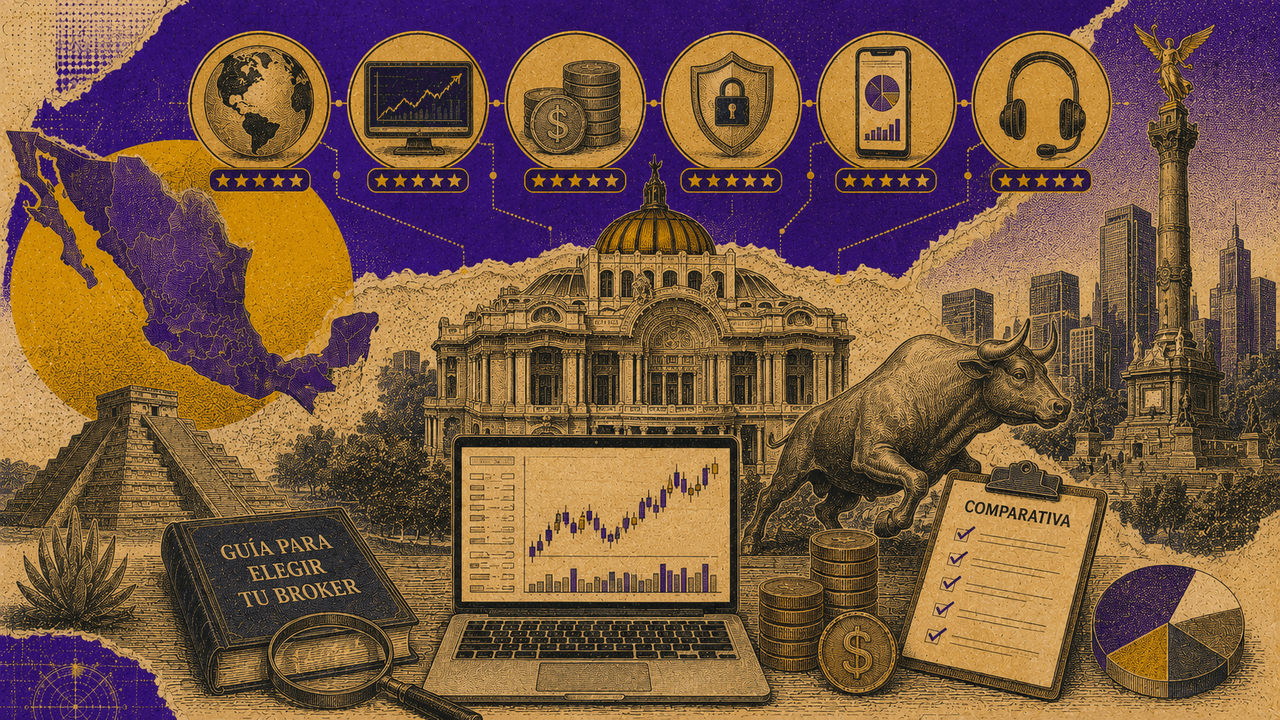

The types of PPR (and where the trap is)

Not all PPRs are the same, and this is where beginners most often go wrong. Broadly, there are three types: those offered by a brokerage or investment platform (funds, stocks, ETFs, with low and transparent fees, suited to people who want low costs and control); those offered by a bank (the bank's own funds, with variable fees worth checking, aimed at customers who want convenience); and those offered by an insurer, sometimes bundled with an insurance policy (a mixed or insurance-linked structure, fees that tend to be high, less liquidity, and only right for specific cases and with caution).

Fees are what most affect your returns over 20 or 30 years. A difference of 1% or 2% per year in fees, compounded over decades, can cost you hundreds of thousands of pesos. That is why comparing the total cost of each PPR matters more than any other feature. The specific fee that eats returns is the expense ratio, so make sure you understand it before signing anything.

How to choose a good PPR

Before you sign up, compare these four points across your options.

Fees: the total annual cost (administration plus management). The lower, the better, especially over the long run.

What it invests in: from conservative (debt) to aggressive (equities). Choose based on your age and your risk tolerance - the further you are from retirement, the more growth makes sense.

Flexibility: can you change your contributions, pause them, or adjust the strategy without a penalty?

Strength and regulation: make sure the institution is regulated, by the CNBV, CNSF, or Condusef depending on the type.

How to start, step by step

Decide how much you can contribute per year without straining your finances - remember, this is long-term money.

Compare at least three PPRs on fees, investment options, and flexibility.

Open the account with your chosen institution; many processes today are fully digital.

Contribute during the year - it can be on a regular schedule - and keep your receipts.

On your annual return (April), deduct your contributions to claim your tax benefit.

The fine print: what happens if you withdraw early

The PPR tax benefit comes with a condition: it is money for retirement, available from age 65, or in cases of disability or incapacity. If you withdraw the money before meeting the requirements, you lose the tax benefit, and the withdrawal is subject to ISR - there is usually a withholding of around 20% on the amount withdrawn.

For that reason, a PPR is not for your emergency fund or for short-term goals. Only contribute money you can genuinely leave invested for years. No investment is without risk, and a long horizon does not remove that - it simply gives your savings more time to ride out the ups and downs.

Frequently asked questions

Is having a PPR mandatory?

No. It is entirely voluntary. Your mandatory retirement account is the AFORE; the PPR is additional savings that you choose to open.

How much can I deduct from my taxes?

Up to the lower of: 10% of your annual income, or 5 UMA per year (around 213,900 MXN in 2026, an approximate figure). Confirm the current limit and check it with an accountant.

Can I take my money out before retirement?

Yes, but you lose the tax benefit and the withdrawal is subject to ISR - there is usually a withholding of around 20%. It is not a good idea to use it for the short term.

PPR or voluntary contributions in my AFORE?

Both can be deductible. The PPR usually offers more investment options; the AFORE offers more convenience. Compare fees in both cases.

How much do I need to start?

It depends on the institution; some platforms allow low amounts and periodic contributions. What matters is consistency, not starting with a large sum.

Legal Notice: Education, not advice. Past results do not guarantee future returns. Investing always involves risks.